For

For

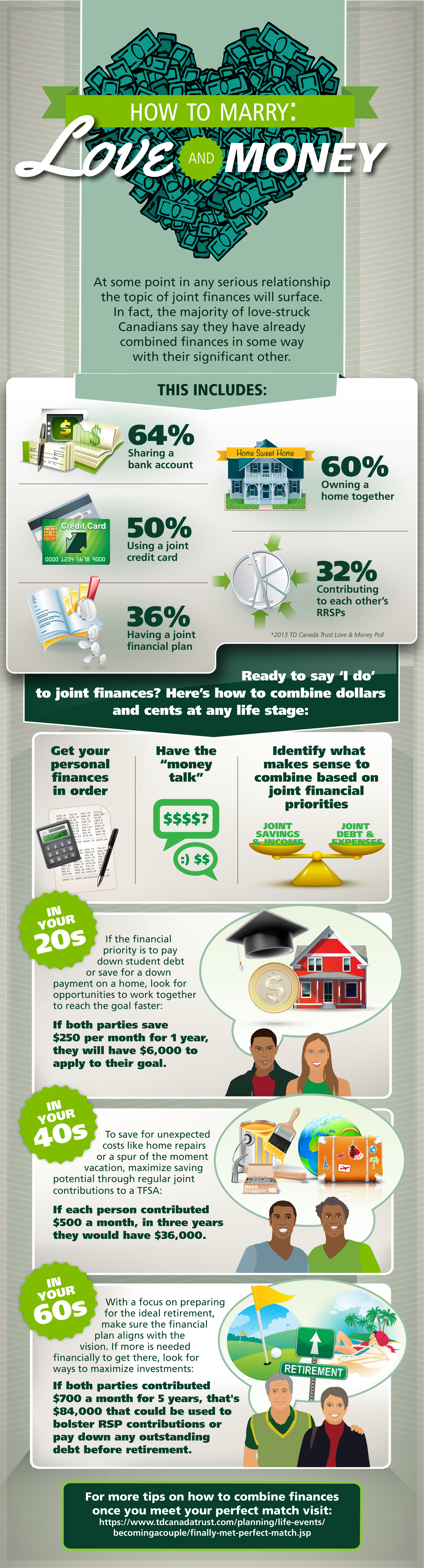

We’ve chosen not to go the route of 64% of couples.

Every week, I get dozens of press releases from media professionals across the country looking to have their story featured on MoneySense.ca. Some are about new products, others are about upcoming events but the vast majority are findings from some survey or other. I pay most attention to the ones that cast the spotlight on some piece of information that you, dear reader, may find helpful on your personal journey to financial independence. This week however a press release on the topic of love and money caught my eye and entirely for selfish reasons: I’m getting hitched in 6 weeks.

TD Canada Trust surveyed adults in committed relationships and found 79% of Canadian couples have joint finances; no surprise there. But here’s where it gets interesting, well for me anyway. The top three personal finance products that Canadians combine with their partner are a joint bank account (64%), a mortgage (60%) and a joint credit card (50%), the bank found. Looks like my husband-to-be and I are taking the road less travelled.

Sure, I’ll be adopting a portion of the mortgage on Michael’s (and soon our) home. But unlike the majority of respondents to the TD poll, we recently made the decision not to open a joint bank account to pay for household expenses like groceries and utilities since neither of us is comfortable closing our existing accounts in favour of a single joint account. After discussing the logistics and monthly fees involved in transferring money from two individual accounts into a third account, we came to the conclusion that it just wouldn’t pay.

Instead, we thought, why not open a joint credit card to pay for all shared expenses? It’s convenient and reduces transaction costs. It also allows us to adjust our individual contributions from month-to-month. We suspect it’ll take a few months for us to determine exactly how much I’ll be contributing to the monthly bills anyway. You see, Michael is used to carrying the cost of the house on his own while I’ve grown accustomed to aggressively saving and budgeting for the odd luxury item (oh the spoils of living at home). We’re both looking forward to this new financial chapter of our lives and realizing our goals together. Ideally, we’d like to accelerate our mortgage payments but not at the expense of my retirement savings for instance. Realistically, we’re not going to achieve the perfect balance right off the bat. Paying the bills from a joint credit card will allow us to track our monthly expenses and test various splits as we go.

Of course this strategy means we’ll have to be extra diligent about paying off our bill to avoid costly interest fees, but neither of us carry a monthly balance on our credit cards so it really doesn’t require a change in habits. And we’ll be able to earn cash-back by paying with a reward credit card which should in theory help us reduce our monthly bills.

Meanwhile, I’ll transfer my share of the mortgage to Michael in lump sums and he’ll continue to pay the mortgage from his existing account. From our perspective it’s a very cost-conscious approach. But we’re clearly not in the majority here so I figured I’d consult TD’s Janice Farrell Jones for a second opinion.

“I wouldn’t say that there’s necessarily any real flaw in your strategy,” she said. “It is a good place to start with one product first, learn about each other that way and go from there.”

Jones also stressed the importance of clearly defining what our joint credit card should be used for. “What are you looking to spend on and do you have the same views on spending habits. Would you treat (the card) the same way?”

If there’s anything the study shows is that there’s no one-size-fits-all approach and we’re on the right track, Jones said, adding that a financial plan is key regardless of how we decide to combine our finances.

“A financial plan is really what’s helping you toward those long-term goals. If you are in a long-term, committed relationship, that’s likely what’s going to matter most down the road,” she said. The TD study found only 36% of Canadian couples have a common financial plan.